Written by VERIFIED Crypto Checkout | Payment Routing & Settlement Infrastructure

How to Accept Payments Without a Merchant Account (WooCommerce Guide)

Merchants usually search for how to accept payments without a merchant account when traditional processing has become unstable, unavailable, or too restrictive for their business model. In practice, this does not mean skipping payment rules. It means using a different payment architecture where a hosted provider handles card processing, compliance, and conversion while the merchant receives settlement through a separate infrastructure layer.

For WooCommerce stores, this can be a practical way to accept card payments when applying for a traditional merchant account is slow, expensive, or unrealistic. The result is a system that still lets businesses accept payment from customers online, but without the merchant directly holding the acquiring relationship that normally sits behind standard merchant accounts.

Key Highlights

- A merchant can accept payments online without a traditional merchant account by using hosted payment infrastructure

- The hosted provider handles credit card processing, identity checks, fraud controls, and conversion

- The merchant receives USDC settlement to a Polygon wallet instead of relying on standard card settlement into merchant accounts

- This can be a useful payment solution for businesses that cannot easily open or maintain merchant accounts

- Subscriptions and payment links make it possible to take credit card payments without stored cards or a standard recurring billing setup

- WooCommerce can be configured to route these online transactions through a native payment gateway integration

What Accepting Payments Without a Merchant Account Actually Means

Accepting payments without a merchant account means a business uses a hosted payment flow where a licensed provider processes credit and debit card payments, and the merchant receives separate settlement rather than operating its own direct acquiring relationship.

That definition matters because many merchants think “without a merchant account” means there is no compliance layer involved. That is not how legitimate online payment infrastructure works. In this model, the merchant is not avoiding compliance requirements. The responsibility for card-network compliance, fraud controls, identity verification, and payment processing sits with the hosted on-ramp provider.

In a traditional setup, a business goes through underwriting, opens one of the standard merchant accounts, connects a payment gateway, and uses that stack to process credit card transactions. Funds usually arrive in a business bank account after settlement, often with exposure to reserves, chargebacks, and account reviews.

In a hosted routing model, the structure changes:

- Customer: chooses to pay with credit cards or debit cards through a hosted checkout flow

- Provider: acts as the payment service provider and card processor, handling verification and processing

- Merchant: receives on-chain settlement in USDC without directly holding a merchant account for card processing

So while it is accurate to say you can accept payments without a merchant account, the more precise explanation is that you are using a different routing and settlement architecture.

Why Merchants Look for This

Most businesses do not look for alternatives to merchant accounts unless something has already broken. They may have been rejected by Stripe, shut down by a processor, hit with reserves, or restricted due to category risk.

- Processor shutdowns or account reviews

- Reserve requirements that limit cash flow

- High-risk underwriting restrictions

- Chargeback exposure tied to traditional credit card processing

- Difficulty setting up or maintaining merchant accounts

When that happens, merchants start looking for ways to accept payment that do not rely entirely on maintaining a direct acquiring relationship.

The 3 Main Alternatives to Merchant Accounts

1. High-Risk Merchant Accounts

This is the traditional path adapted for higher-risk businesses.

- Allows direct processing of credit cards

- Often includes higher transaction fees

- May require reserves and monitoring

- Approval timelines can be slow and unstable

2. ACH / eCheck

Bank-based payment methods that bypass card networks.

- Lower chargeback exposure

- Limited adoption compared to credit cards

- Slower settlement

- Less effective for impulse or mobile payment behavior

3. Hosted Card-to-Crypto Checkout

This model allows businesses to accept card payments without maintaining their own merchant account by routing transactions through licensed providers.

- No direct merchant account required

- Global card acceptance through providers

- Settlement in USDC

- Reduced chargeback exposure after settlement

Settlement speed: near real-time after confirmation, compared to multi-day settlement cycles common with traditional merchant accounts.

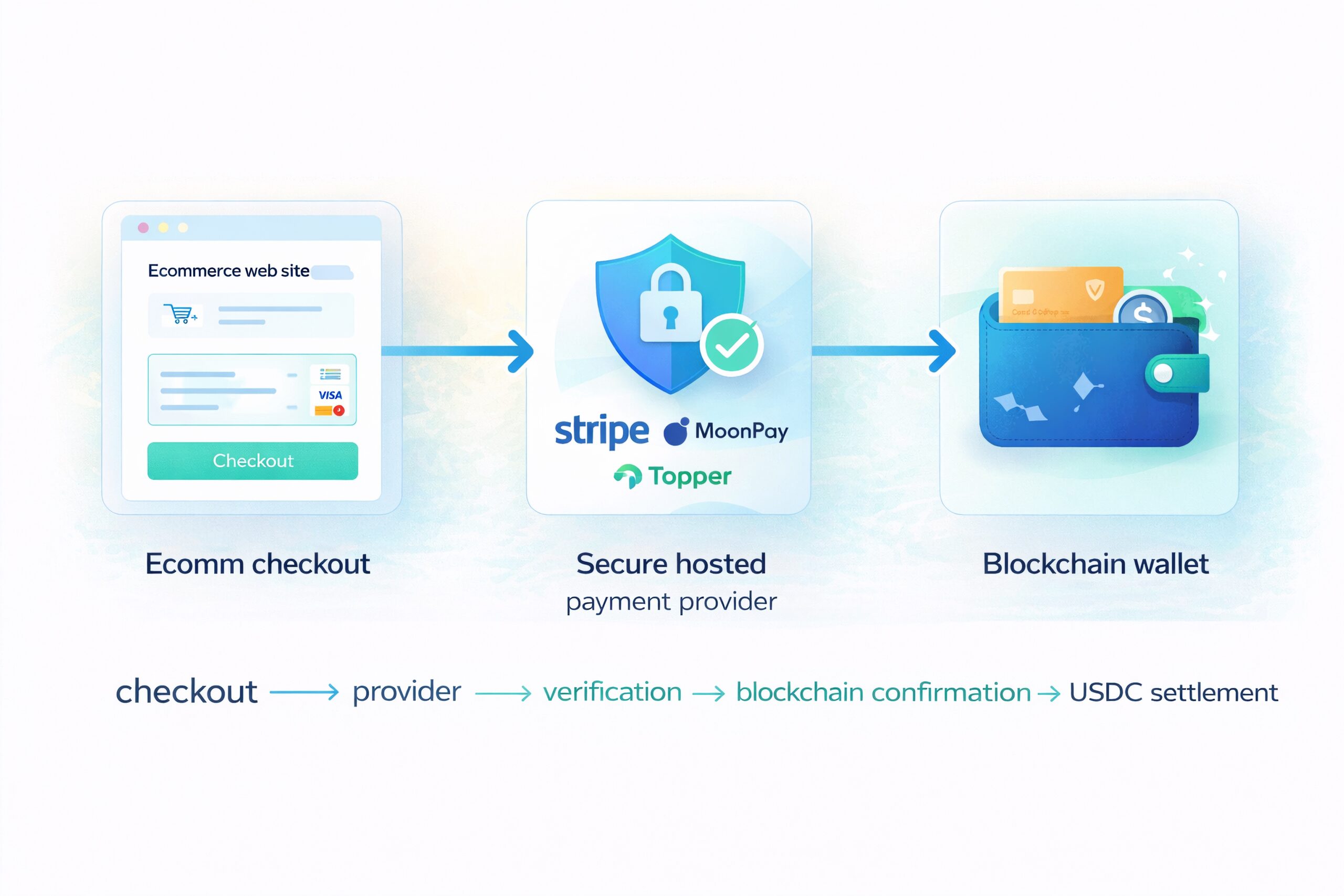

How Hosted Card-to-Crypto Checkout Works

The flow below represents the standard hosted routing model:

- Customer selects the payment option

The WooCommerce checkout presents a hosted payment method. - Redirect to provider

The customer is sent to a secure hosted checkout environment. - Card processing and verification

The provider processes the transaction and may require identity verification. - Conversion to USDC

The payment is converted through the provider’s infrastructure. - On-chain settlement

Funds are delivered to the merchant wallet on Polygon using USDC. - Webhook confirmation

The WooCommerce order updates after confirmation. Our plugin also checks the blockchain if a webhook is not received (this is extra protection beyond most other on ramp plugins).

Once a customer completes verification with a provider, future transactions are often significantly faster. This creates a network effect where repeat buyers experience a much smoother checkout process over time.

Why This Model Works From a Compliance Perspective

This is not a workaround. It is a shift in responsibility.

The hosted provider manages card processing, fraud controls, identity verification, and regulatory requirements. The merchant is using infrastructure that routes payments through that provider rather than directly processing cards.

Because the provider handles the transaction, customer data is processed within the provider’s secure environment, which can reduce the merchant’s direct PCI scope compared to handling card data on-site.

This model operates within existing regulatory frameworks by relying on licensed providers that handle conversion and compliance in their respective jurisdictions.

Where Subscriptions Fit

Traditional subscription billing relies on stored cards and recurring charges, which require stable merchant accounts.

This routing model uses renewal links instead:

- No stored card data

- No automatic rebilling against saved credentials

- Each payment is a new authorized transaction

- Settlement still occurs in USDC

This allows merchants to run subscription-style billing without relying on stored card infrastructure.

Where Payment Links Fit

Payment links extend the system beyond checkout.

- Recover abandoned orders

- Send invoices directly to customers

- Act as a virtual terminal

- Collect payments without requiring a full checkout flow

This gives merchants a flexible way to accept payment in multiple scenarios.

When This Model Makes Sense

- High-risk ecommerce businesses

- Merchants who have lost or cannot obtain merchant accounts

- Global businesses needing broader payment coverage

- Subscription businesses without stored billing tolerance

- Merchants needing a backup payment rail

When It Doesn’t

- Low-risk businesses with stable merchant accounts

- Merchants requiring fully automatic recurring billing

- Businesses needing direct bank settlement from card processors

- Stores requiring zero checkout redirection

WooCommerce Implementation

Implementation is handled through a WooCommerce payment gateway:

- Install and activate the plugin

- Configure your settlement wallet

- Select routing preferences

- Enable subscriptions or payment links if needed

- Monitor transactions inside WooCommerce

For custom builds or non-WooCommerce environments, the same routing architecture can also be implemented via API, allowing developers to integrate hosted payment flows into custom checkout systems while maintaining the same settlement model.

Compatible with modern WooCommerce environments, including block-based checkout systems.

Operational Note

Operational note: Many merchants use this architecture as a continuity layer. If a primary processor places an account under review or restricts activity, this hosted routing model can remain active as an alternative checkout path.

System Positioning

VERIFIED Crypto Checkout operates as a routing layer inside WooCommerce. It connects merchants to on-ramp providers and manages the flow between checkout and settlement.

Verified Credit Card Processing focuses on underwriting and merchant accounts, while VERIFIED Crypto Checkout provides the infrastructure for alternative routing when those options are unavailable.

Final Thoughts

There is no way to accept payments without infrastructure. When merchant accounts fail, the solution is not to remove the system, but to change how payments are routed and settled.

This hosted model gives WooCommerce merchants a way to keep accepting payments, maintain continuity, and operate outside the limitations of traditional merchant account structures.

Frequently Asked Questions

Can you accept payments without a merchant account?

Yes. Payments can be processed through a hosted provider that handles the transaction, while the merchant receives settlement separately. This allows businesses to operate without maintaining their own merchant account.

Can WooCommerce accept credit card payments without a merchant account?

Yes. WooCommerce can use hosted payment routing where customers complete payment on a provider page, allowing merchants to accept card payments without directly holding a merchant account.

Is this a compliant way to process payments?

Yes. Licensed providers handle compliance, fraud checks, and identity verification. The merchant is using infrastructure to route payments, not bypassing regulations.